Understanding the Green Card Exit Tax: Key Considerations for Expats

Written by John Woodfield Portfolio Manager, CFP®, CIM® and Tiffany Woodfield, TEP, Associate Portfolio Manager, CRPC®, CIM®

Green Card Exit Tax and the 8-Year Rule: What You Need to Know

Renouncing your Green Card is a major life decision, and for long-term residents, it can come with significant financial implications. Chief among these is the Green Card Exit Tax, often referred to as the expatriation tax.

The 8-Year Rule means that a lawful permanent resident is classified as a long-term resident if they have held a Green Card for 8 out of the last 15 tax years, even if they didn’t physically live in the U.S. during that entire period. If you are a lawful permanent resident, then you will may have to pay exit taxes. Speak to a cross-border lawyer and accountant if you’re unsure about your situation.

As cross-border financial advisors based in Canada, we focus on how the exit tax affects Green Card holders transitioning to Canadian residency. Strategic planning is essential to ensure compliance with U.S. tax laws while minimizing unexpected liabilities. We recommend that you seek the assistance of a cross-border advisor and accountant before you move if you wish to minimize taxes. This article is for information purposes only, please speak to an advisor and accountant about your situation.

Table of Contents

- What Is the Exit Tax?

- Are You a Covered Expatriate?

- How the Exit Tax is Calculated

- What Is the 8-Year Rule?

- Why Is the 8-Year Rule Important?

- How the 8-Year Period Is Calculated

- Practical Implications of the 8-Year Rule

- Cross-Border Tax Considerations

- Strategies to Minimize the Exit Tax

- Exceptions for Dual Citizens and Minors

- Why Work with a Cross-Border Advisor?

- Q & A about the Green Card Exit Tax

What Is the Exit Tax?

The exit tax applies to individuals classified as covered expatriates. For Green Card holders, the key trigger to being considered an expatriate is giving up your green card after having maintained lawful permanent resident (LPR) status for 8 of the last 15 tax years. (+) Then you need to consider if you may be considered a covered expatriate because this can result in a large tax bill.

If you qualify as a covered expatriate, the IRS treats your worldwide assets as if they were sold at fair market value the day before expatriation. This “deemed sale” (a deemed disposition) can result in capital gains taxes on unrealized gains. It can also result in immediate taxation on certain types of deferred compensation and trust distributions.

Are You a Covered Expatriate?

You’re considered a covered expatriate if you meet any of the following criteria:

- Net Worth Test: Your net worth is $2 million or more on your expatriation date.

- Tax Liability Test: Your average annual net income tax liability for the five years prior to expatriation exceeds $206,000 (for 2025; adjusted annually for inflation).

- Certification Test: You fail to certify on Form 8854 that you have complied with all U.S. federal tax obligations for the five years preceding expatriation.

It’s worth noting that if you are a U.S. citizen and moving to Canada but not giving up your U.S. citizenship then you are not expatriating and therefore cannot be a covered expatriate. Also there are some exceptions, where you can be exempt from covered expatriate status. (+)

How the Exit Tax is Calculated

For covered expatriates, the exit tax involves:

- Mark-to-Market Taxation

- Deferred Compensation

- Trusts

1 - Mark-to-Market Taxation:

All worldwide assets are treated as if sold for their fair market value the day before expatriation. For 2024, the first $866,000 of capital gains is excluded from taxation (adjusted annually for inflation).

Mark-to-market taxation example:

Under the exit tax rules, all worldwide assets of a covered expatriate are generally treated as if sold for their fair market value the day before expatriation. This deemed sale triggers a capital gains tax on unrealized gains above a specific exclusion threshold.

Let’s say your investment portfolio has unrealized gains of $1.5 million. The exclusion amount for 2024 is $866,000. This means $634,000 of gains would be subject to capital gains tax. If the applicable tax rate is 20%, you would owe $126,800 in exit tax on the portfolio alone.

This simplified example highlights the potential impact of mark-to-market taxation, emphasizing the importance of planning to mitigate this liability. Speak to your cross-border team to determine how this works.

2 - Deferred Compensation:

Deferred compensation accounts like pensions and vested stock options are treated as if distributed on the day before expatriation, triggering an immediate tax liability.

Eligible deferred compensation plans (e.g., 401k, 403b) are subject to a 30% withholding tax on distributions after expatriation.

3 - Trusts:

Distributions from non-grantor trusts are usually subject to immediate taxation.

What Is the 8-Year Rule?

The 8-Year Rule is a key provision in U.S. tax law that applies to Green Card holders who are considering expatriation. Under this rule, a lawful permanent resident (Green Card holder) is classified as a long-term resident if they have held a Green Card for 8 out of the last 15 tax years, even if they didn’t physically live in the U.S. during that entire period. Speak to your accountant to determine if you are a long-term resident.

Why Is the 8-Year Rule Important?

Being classified as a long-term resident under the 8-Year Rule has significant tax implications:

- Covered Expatriate Status:

If a long-term resident decides to relinquish their Green Card, they may be subject to the exit tax if they meet certain criteria (net worth over $2 million, average annual tax liability exceeding a threshold, or failure to certify tax compliance). - Triggering the Exit Tax:

For long-term residents, relinquishing a Green Card is considered expatriation. This means they are subject to U.S. tax rules that treat their worldwide assets as if sold at fair market value (mark-to-market taxation), potentially triggering capital gains taxes. - Exemptions:

If you have held a Green Card for fewer than 8 years, you likely are not classified as a long-term resident, and the exit tax does not apply when you relinquish your Green Card.

How the 8-Year Period Is Calculated

- The 8 years don’t have to be consecutive.

- Even a partial year in which you were a Green Card holder counts as a full year.

- The count is based on tax years, not calendar years (i.e., January 1 to December 31).

Speak to your tax advisor to understand if you may be considered a long-term resident.

Practical Implications of the 8-Year Rule

For Green Card holders approaching the 8-year mark, timing is critical. If you’re considering relinquishing your Green Card, doing so before reaching 8 years of U.S. tax residency can help you avoid being classified as a long-term resident and potentially subject to the exit tax.

This rule underscores the importance of strategic tax planning and consulting with a cross-border advisor and accountant to navigate these complex regulations.

Cross-Border Tax Considerations

For Green Card holders moving to Canada, it’s important to understand how the U.S. and Canadian tax systems interact.

U.S. Tax Residency Rules: Green card holders are considered U.S. tax residents and must report their worldwide income to the IRS, even if living abroad. Filing Form 1040 annually is required.

Canadian Tax Residency Rules: Canada taxes are based on residency. If you’re a Canadian resident, you’ll need to report your worldwide income to the CRA.

Avoiding Double Taxation: The Canada-U.S. Tax Treaty helps avoid double taxation by determining residency status and allowing foreign tax credits for taxes paid in one country on income earned in the other.

Understanding the interplay of these systems is crucial to maintaining compliance and minimizing your tax burden during this transition.

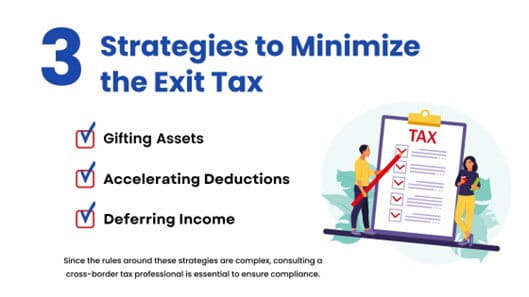

Strategies to Minimize the Exit Tax

If you anticipate being classified as a covered expatriate, advanced tax planning can help mitigate the exit tax. Here are a few strategies to consider:

- Gifting Assets: Transferring assets to family members or trusts before expatriation can reduce your net worth below the $2 million threshold, avoiding covered expatriate status.

- Accelerating Deductions: Maximizing deductions prior to expatriation can lower your average annual tax liability, potentially helping you pass the tax liability test.

- Deferring Income: Timing income recognition for after expatriation may reduce your taxable income in the U.S.

Since the rules around these strategies are complex, consulting a cross-border tax professional is essential to ensure compliance.

Exceptions for Dual Citizens and Minors

Not all Green Card holders are subject to the exit tax. Exceptions apply to:

- Dual Citizens:

If you were born with dual citizenship and have been a U.S. resident for no more than 10 years in the past 15 years, you may be exempt from covered expatriate status. - Minors:

If you renounce your Green Card before turning 18 ½ and have not been a U.S. resident for more than 10 years, you may also qualify for an exception.

These exemptions underscore the importance of tailored tax advice based on your unique circumstances.

Why Work with a Cross-Border Advisor?

The financial implications of the exit tax are complex and far-reaching. Without proper planning, Green Card holders can face significant tax liabilities that reduce their wealth.

By working with a dual-licensed cross-border advisor, you gain access to:

- Expertise in navigating U.S. and Canadian tax laws.

- Comprehensive financial strategies to minimize tax exposure.

- Peace of mind during a potentially stressful transition.

Whether you’re considering relinquishing your Green Card or exploring cross-border residency options, seeking professional advice is the key to protecting your wealth and ensuring compliance with U.S. and Canadian tax systems.

Questions about the Green Card Exit Tax

How does my permanent resident status affect my U.S. tax obligations and the exit tax?

Holding permanent resident status (a Green Card) means you are considered a U.S. tax resident and required to report worldwide income annually on Form 1040. If you maintain this status for 8 of the last 15 tax years, you may qualify as a long-term resident under U.S. tax law. Long-term residents who relinquish their Green Card may be classified as covered expatriates, triggering the exit tax on unrealized gains and certain deferred compensation.

What role does average net income tax play in determining covered expatriate status?

One test for becoming a covered expatriate is whether your average annual net income tax liability exceeds a set threshold ($206,000 for 2025). This figure reflects your U.S. tax obligations over the five years prior to expatriation. If your tax liability surpasses this amount, you may be subject to the exit tax, which involves taxation on worldwide assets as though they were sold the day before expatriation.

What reporting obligations do Green Card holders face when relinquishing permanent resident status?

Relinquishing a Green Card requires filing Form I-407 (to formally surrender permanent resident status) and Form 8854 (to certify compliance with U.S. tax obligations).

Form 8854 determines whether you are a covered expatriate and subject to the exit tax. Additionally, you must have filed accurate tax returns for the five years preceding expatriation. Failure to meet these obligations could result in penalties or automatic classification as a covered expatriate.

Final Thoughts

The Green Card Exit Tax presents significant challenges, but with proactive planning and expert guidance, you can make informed decisions that safeguard your financial future. By understanding the rules, leveraging tax treaty provisions, and implementing strategic solutions, you can transition to Canadian residency with confidence.

If you’re ready to explore your options, consult with a cross-border financial advisor today. The complexities of cross-border tax law are too great to navigate alone—don’t leave your wealth to chance.

Next Steps

If you’re a Canadian resident or are planning on moving to Canada or the US and need assistance with moving and optimizing your investments, estate planning, wealth management and portfolio management, please get in touch. At SWAN Wealth, we specialize in Canadian financial planning, cross-border financial planning and cross-border wealth management.

Cross-Border Advisor - Make Sure You Watch This

Read More

If you’re planning a cross-border move, these articles and guides will help simplify your move and ensure you’ve covered everything.

- Do Dual Citizens Pay Taxes in Both Countries?

- How to Move to Canada from the US

- How Hard Is It to Move to Canada?

- The Cost of Renouncing Your U.S. Citizenship

About the Authors

Tiffany Woodfield is an Associate Portfolio Manager licensed in Canada and the USA, a Chartered Investment Manager (CIM), a Chartered Retirement Planning Counselor (CRPC), a Trust and Estate Practitioner (TEP) and the co-founder of SWAN Wealth Management, along with her husband, John Woodfield. Tiffany advises clients who live in Canada and the United States and want to simplify their cross-border financial plan, move their assets across the border, and optimize their investments to minimize their tax burden. Together, Tiffany and John Woodfield help their clients simplify their cross-border finances and create long-term revenue streams that will keep their assets safe whether they live in Canada or the U.S.

John Woodfield is a Financial Management Advisor (FMA), a Chartered Investment Manager (CIM), and a Certified Financial Planner (CFP), and in 2007 was inducted as a fellow of the Canadian Securities Institute (FCSI). As a portfolio manager and CFP®, he works with clients across Canada. John Woodfield’s clients are families, individuals and business owners who understand the importance of comprehensive wealth and investment plans driven by the lifestyle they want to lead.

Schedule a Call

Schedule a 15-minute introductory call with SWAN Wealth Management.

Click here to schedule a call.

![]()