How to Avoid Capital Gains Tax on Employee Stock Options as a Green Card Holder Moving to Canada

Written by John Woodfield Portfolio Manager, CFP®, CIM® and Tiffany Woodfield, TEP, Associate Portfolio Manager, CRPC®, CIM®

The Canada-U.S. Tax Treaty plays a pivotal role in determining the tax obligations of U.S. citizens and Green Card holders who live or plan to live in Canada.

Navigating these complexities is particularly important for individuals with employee stock options, as tax implications can vary significantly depending on where you reside when those options vest or are exercised. Understanding how to avoid capital gains tax on stock options is crucial for minimizing your tax liabilities.

This blog outlines key considerations, strategies, and the importance of working with a cross-border financial team to optimize your outcomes.

This information is not meant as advice and is general in nature you need to speak to your cross-border team about your particular situation.

Table of Contents

- What Is Capital Gains Tax?

- How Are Employee Stock Options Taxed?

- Strategies to Minimize Capital Gains Tax on Stock Options

- Special Considerations for Green Card Holders

- Tax-Efficient Investment Strategies

- Using Fair Market Value to Your Advantage

What Is Capital Gains Tax?

Capital gains tax is levied on the profit realized from selling a capital asset, such as stocks or real estate. While the U.S. and Canada both tax capital gains, the rules governing their calculation and timing differ:

- U.S. Tax System: The holding period (short-term vs. long-term) impacts the tax rate. Gains from assets held for over a year benefit from lower long-term capital gains tax rates.

- Canadian Tax System: Only 50% of capital gains are taxable, but all gains, regardless of the holding period, are taxed at your marginal tax rate.

When dealing with stock options, understanding these differences and leveraging strategies to reduce your tax burden is essential. (+)

How Are Employee Stock Options Taxed?

The taxation of employee stock options depends on their classification and the country in which they are taxed. Here's a breakdown:

U.S. Taxation of ESOs

Incentive Stock Options (ISOs):

- No tax at the time of grant or exercise.

- The difference between the exercise price and the fair market value at exercise is subject to the Alternative Minimum Tax (AMT).

- Gains are taxed at long-term capital gains rates if held for at least one year post-exercise and two years post-grant. Otherwise, they are taxed as ordinary income.

Non-Qualified Stock Options (NSOs):

- Taxed at exercise based on the difference between the exercise price and the fair market value.

- Any subsequent gain or loss is treated as a capital gain or loss upon sale.

Canadian Taxation of ESOs

Canadian-Controlled Private Corporation (CCPC) Stock Options:

- No tax at grant or exercise.

- Taxes are paid when the shares are sold, with a 50% deduction on the taxable gain under certain conditions.

Non-CCPC Stock Options:

- Tax is applied in the year of exercise based on the difference between the exercise price and the fair market value.

- A 50% deduction may apply if specific criteria are met.

Key Differences Between Tax Treatment in Canada and the U.S

- In the U.S., ISOs can defer taxation until the stock is sold, while NSOs trigger taxation at exercise.

- In Canada, CCPC stock options allow for deferral until the sale, while non-CCPC options are taxed at exercise.

Strategies to Minimize Capital Gains Tax on Stock Options

Timing Your Exercise and Sale

For U.S. citizens or Green Card holders planning to move to Canada, timing the exercise or sale of stock options can reduce or eliminate exposure to capital gains tax. Strategic timing ensures gains are taxed in the jurisdiction with more favourable tax treatment.

Leveraging Fair Market Value

The fair market value (FMV) of your assets at the time of expatriation can be reset as the cost basis for Canadian tax purposes. Proper planning can prevent double taxation by using this reset value to align your tax liabilities.

Planning Around the Expatriation Tax

If you are a long-term U.S. resident (holding a Green Card for eight out of 15 years), relinquishing your status may trigger the expatriation tax. This tax treats your worldwide assets as if sold the day before expatriation, potentially incurring a significant liability. Proper structuring and advice can help mitigate these impacts.

Utilizing Cross-Border Investment Expertise

A cross-border financial team can help coordinate investment structures, stock option exercises, and tax residency transitions. Advisors work with tax professionals to optimize deductions, exemptions, and treaties that reduce your overall tax burden.

Special Considerations for Green Card Holders

Green Card Status and Tax Obligations

Green Card holders are subject to U.S. taxes on worldwide income, even if residing abroad. Expatriation taxes may apply if the Green Card is relinquished after meeting the long-term residency test.

Covered Expatriates

If classified as a "covered expatriate," you may face an exit tax upon relinquishing your Green Card or U.S. citizenship. This includes stock options and other capital assets. (+)

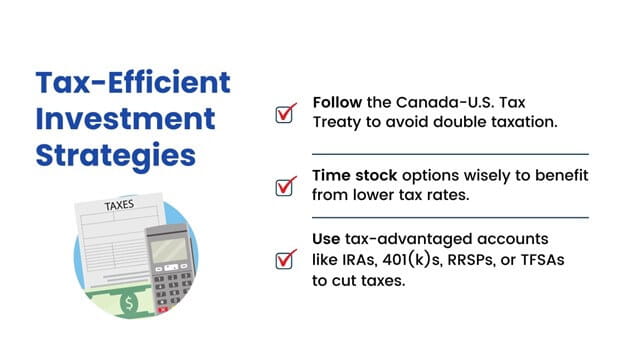

Tax-Efficient Investment Strategies

Those who do not have to pay an exit tax, especially those who have held a Green Card for less than eight of the last 15 years, can benefit from strategic capital gains tax planning. Capital gains accrued before returning to Canada and becoming solely a Canadian tax resident may be exempt from U.S. or Canadian taxation. You need to speak to a cross-border professional about your particular situation.

For those with high-value employee stock options, strategic tax planning is critical. Here are a few approaches:

- Coordinate with the Canada-U.S. Tax Treaty: This treaty helps mitigate double taxation on gains, but proper filing is essential.

- Optimize Stock Option Timing: Plan the exercise and sale of options to take advantage of preferential tax rates.

- Use Tax-Efficient Accounts: Leveraging U.S. and Canadian tax-advantaged accounts, such as IRAs, 401(k)s, RRSPs, or TFSAs, can reduce taxable income.

Using Fair Market Value to Your Advantage

The fair market value, when expatriating, can become the new cost basis for taxable capital gains for Canadian tax purposes, potentially eliminating further U.S. taxes on taxable income and avoiding Canadian taxes on accrued investment gains. With proper planning and professional advice, steps can be taken to reduce the tax burden on your stock options.

Why You Need Cross-Border Advisors

Employee stock options are a valuable asset, but navigating their taxation is complicated when crossing the Canada-U.S. border. Working with a dual-licensed cross-border advisor ensures your financial plan is optimized. A cross-border team collaborates with specialized tax accountants and legal professionals to address:

- Compliance with both U.S. and Canadian tax laws.

- Strategies to defer or reduce taxation on stock options.

- Planning for expatriation or changes in residency.

Without this expertise, you risk unnecessary taxation and compliance issues.

Moving from the USA to Canada as an American - Critical Info!

The Bottom Line

Reducing capital gains tax on stock options requires careful planning, particularly for Green Card holders or U.S. citizens moving to Canada. Key steps include understanding the tax rules in both countries, strategically timing exercises and sales, and working with a qualified cross-border financial team.

For those facing complex scenarios, professional guidance isn’t just helpful—it’s essential. By partnering with cross-border specialists, you can protect your wealth and achieve long-term financial security while minimizing your tax burden.

Q & A

What are short-term capital gains?

Short-term capital gains are profits from assets held for one year or less, taxed at the higher ordinary income tax rate.

Is a tax advisor important for managing capital gains taxes on investments?

Yes, a tax advisor helps optimize tax strategies, ensuring compliance and reducing liabilities, especially for complex situations like stock options.

How can you lower ordinary income taxes on stock options while managing investment risks?

Strategically timing exercises, selling options at favourable rates, and leveraging tax deductions can lower ordinary income taxes while mitigating risks.

How does the capital gains tax rate impact your investment strategy, knowing that investing involves risk?

Lower long-term capital gains tax rates encourage holding investments longer, balancing risk and potential tax savings.

Are there differences in how capital gains taxes apply to Incentive Stock Options (ISOs) versus Non-Qualified Stock Options (NSOs)?

Yes, ISOs can qualify for long-term capital gains rates, while NSOs are taxed as ordinary income at exercise, with gains/losses taxed at sale.

How can the timing of exercising and selling stock options affect your capital gains tax liability?

Timing can shift taxes from higher short-term rates to lower long-term rates, significantly affecting your tax liability.

What happens to capital gains taxes if you move to another country, like Canada, before exercising or selling stock options?

Tax residency changes can alter tax obligations, potentially exposing you to taxation in both countries without proper planning.

How does the Alternative Minimum Tax (AMT) affect stock options and capital gains tax planning?

The AMT can create additional tax liabilities for ISOs by taxing the difference between the exercise price and fair market value.

Next Steps

If you’re a Canadian resident or are planning on moving to Canada or the US and need assistance with moving and optimizing your investments, estate planning, wealth management and portfolio management, please get in touch. At SWAN Wealth, we specialize in Canadian financial planning, cross-border financial planning and cross-border wealth management.

Read More

If you’re planning a cross-border move, these articles and guides will help simplify your move and ensure you’ve covered everything.

- US Taxes in Canada

- Do Dual Citizens Pay Taxes in Both Countries?

- Moving to Canada from the US

- Cross-Border Estate Planning Guide

About the Authors

Tiffany Woodfield is an Associate Portfolio Manager licensed in Canada and the USA, a Chartered Investment Manager (CIM), a Chartered Retirement Planning Counselor (CRPC), a Trust and Estate Practitioner (TEP) and the co-founder of SWAN Wealth Management, along with her husband, John Woodfield. Tiffany advises clients who live in Canada and the United States and want to simplify their cross-border financial plan, move their assets across the border, and optimize their investments to minimize their tax burden. Together, Tiffany and John Woodfield help their clients simplify their cross-border finances and create long-term revenue streams that will keep their assets safe whether they live in Canada or the U.S.

John Woodfield is a Financial Management Advisor (FMA), a Chartered Investment Manager (CIM), and a Certified Financial Planner (CFP), and in 2007 was inducted as a fellow of the Canadian Securities Institute (FCSI). As a portfolio manager and CFP®, he works with clients across Canada. John Woodfield’s clients are families, individuals and business owners who understand the importance of comprehensive wealth and investment plans driven by the lifestyle they want to lead.

Schedule a Call

Schedule a 15-minute introductory call with SWAN Wealth Management.

Click here to schedule a call.

![]()