Are Roth IRA Distributions Taxable?

Written by Tiffany Woodfield, TEP, Associate Portfolio Manager, CRPC®, CIM® and John Woodfield Portfolio Manager, CFP®, CIM®

Q: Are Roth IRA distributions taxable?

Qualified distributions from a Roth IRA are not taxable. But what makes a distribution qualified?

Whether or not Roth IRA distributions are qualified depends on several factors, including how long the account has been open, the type of contribution made, and the reason for the withdrawal.

In this blog, we'll explore the conditions that make a Roth IRA distribution tax-free, the exceptions that may apply, and the crucial differences between qualified and non-qualified distributions.

We aim to provide a clear understanding so you can confidently manage your Roth IRA and its tax implications, whether you're in Canada or the U.S.

This blog is general in nature and you need to speak to your cross-border financial advisor and accountant about your particular situation.

*With some institutions, including Raymond James, you need to have held the Roth IRA for 5 years at Raymond James for the distribution to be exempt from withholding tax.

TABLE OF CONTENTS

- Qualified Distributions

- Non-Qualified Distributions

- Special Considerations for Cross-Border Individuals

- Why Work with a Cross-Border Advisor?

- Key Differences Between Roth IRA and Traditional IRA Distributions

- How to Get the Most Out of Your Roth IRA Withdrawal Strategy

- How Non-Qualified Distributions Are Taxed

- Example of Qualified and Non-Qualified Distributions

- Are You Dealing with a Roth IRA in Canada?

- Common Questions About Taxes on Roth IRA Distributions

Qualified Distributions

Qualified distributions from a Roth IRA are generally not taxable. To qualify:

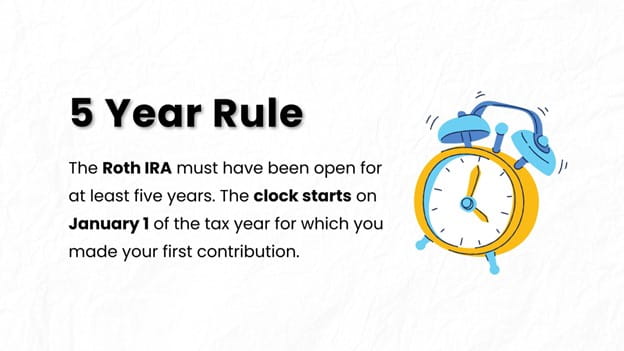

- The Five-Year Rule: The Roth IRA must have been open for at least five years. The clock starts on January 1 of the tax year for which you made your first contribution, or January 1 of the year of conversion.

- Age or Specific Conditions: You must meet at least one of the following conditions:

- Be age 59½ or older.

- Use the funds (up to $10,000 lifetime) for a qualified first-time home purchase.

- Be disabled.

- The distribution is made to your beneficiary or estate after your death.

If both of the above conditions are met, the distribution of both contributions and earnings is generally tax-free.

Non-Qualified Distributions

If you take a distribution that doesn’t meet the above criteria, it may be subject to taxes and possibly a 10% early withdrawal penalty. Here’s how it works:

- Contributions: Roth IRA contributions are made with after-tax dollars, so you can withdraw these contributions anytime, tax-free and penalty-free.

- Earnings: Withdrawals of earnings may be subject to ordinary income tax and a 10% early withdrawal penalty if the distribution is non-qualified.

Special Considerations for Cross-Border Individuals

At SWAN Wealth, we work with cross-border individuals and families with assets in Canada and the U.S. For individuals with cross-border ties between the U.S. and Canada, the tax treatment of Roth IRA distributions can become more complicated.

1 - Canada’s Perspective on Roth IRAs:

- In most cases, Roth IRAs are not recognized as tax-free accounts in Canada unless specific treaty elections are made.

- Without the treaty election, earnings may be taxable in Canada even if they are tax-free in the U.S.

- The treaty election in Canada refers to filing a one-time declaration under Article XVIII(7) of the Canada-U.S. Tax Treaty to exempt Roth IRA growth and distributions from Canadian taxation, provided specific conditions are met.

2 - Treaty Benefits:

- Under the Canada-U.S. Tax Treaty, Roth IRA distributions may be tax-free in Canada if you have satisfied the same conditions required for tax-free treatment in the U.S. and you do not contribute to the Roth IRA while resident in Canada.

- It’s critical to work with a cross-border financial advisor and tax advisor to ensure proper treaty elections are filed to preserve the tax-free nature of the account.

3 - Residency and Reporting:

- Dual citizens who’ve moved back to Canada must carefully navigate reporting requirements in both countries, including filing the appropriate forms to avoid double taxation or penalties.

Why Work with a Cross-Border Advisor?

If you’re managing a Roth IRA and have cross-border ties, the stakes are high.

Missteps in understanding the tax implications could lead to unexpected tax liabilities or penalties. A cross-border financial advisor can help you:

- Assess the tax implications of distributions in both countries.

- Navigate treaty provisions and filing requirements.

- Incorporate your Roth IRA into a comprehensive cross-border financial strategy that is optimized for your residency.

Key Differences Between Roth IRA and Traditional IRA Distributions

The key difference between Roth IRA and Traditional IRA distributions lies in their tax treatment and timing.

Roth IRA distributions are generally tax-free, provided the account has been open for at least five years, and the account holder is 59½ or older, offering significant tax advantages during retirement. (See the previous paragraph on what makes a distribution qualified.)

Contributions to a Roth IRA are made with after-tax dollars, so withdrawals of contributions are always tax-free. In contrast, Traditional IRA distributions are taxed as ordinary income since contributions are typically made pre-tax or tax-deductible. However, it is possible to have non-deductible contributions in a traditional IRA, which requires careful tracking and reporting of the cost basis.

Additionally, Traditional IRAs require mandatory distributions starting at age 73 (as of 2023), known as Required Minimum Distributions (RMDs), whereas Roth IRAs do not have RMDs during the account holder's lifetime, allowing greater flexibility in retirement planning.

How to Get the Most Out of Your Roth IRA Withdrawal Strategy

To maximize the benefits of your Roth IRA withdrawal strategy, prioritize keeping the account intact as long as possible to take advantage of tax-free compounding growth.

Roth IRAs have no Required Minimum Distributions (RMDs) during your lifetime, so you can keep them intact for as long as required. Consider using your Roth IRA as a later-stage resource in retirement, drawing first from taxable, and Traditional IRA accounts to minimize taxable income and allow the Roth funds to grow.

Ensure you meet the five-year rule and age 59½ requirement for qualified distributions to avoid taxes on earnings.

Finally, if you have cross-border financial ties, work with a cross-border advisor and accountant to file the necessary treaty elections and align your withdrawals with tax rules in both countries. Thoughtful coordination with a comprehensive financial plan can maximize the Roth IRA’s role in preserving your wealth and providing tax-efficient income.

How Non-Qualified Distributions Are Taxed

Non-qualified distributions from a Roth IRA are taxed and penalized based on the IRS ordering rules, which determine the sequence in which funds are withdrawn from the account.

Distributions are taken in the following order:

- Contributions: Contributions are always withdrawn first, tax-free and penalty-free, since they were made with after-tax dollars.

- Conversions: Next, funds from Roth IRA conversions are withdrawn. These are tax-free as long as taxes were paid at the time of conversion, but if the withdrawal occurs within five years of the conversion and the account holder is under 59½, a 10% early withdrawal penalty may apply.

- Earnings: Lastly, earnings on contributions and conversions are withdrawn. Earnings are subject to ordinary income tax if the distribution is non-qualified and may also incur a 10% early withdrawal penalty if the account holder is under 59½.

Certain exceptions, such as disability, qualified education expenses, or first-time home purchases (up to $10,000), may waive the 10% penalty but do not exempt the earnings from income tax. A last resort strategy that anyone can use to avoid the 10% early withdrawal penalty is to receive distributions as part of a series of substantially equal payments for at least five years, known as the 72(t) rule. This nuanced taxation structure highlights the importance of understanding the rules before taking non-qualified distributions to avoid unexpected tax liabilities and penalties.

Review full details on the IRS Website's Roth IRA information page.

Example of Qualified and Non-Qualified Distributions

Here are a few scenarios to illustrate how Roth IRA withdrawals work. See if your particular situation is covered. And remember, it's important to work with a financial advisor and accountant to understand your situation.

Example 1: Tax-Free Qualified Distribution

Jane, age 63, has had her Roth IRA open for 12 years. Her account is valued at $400,000, consisting of $250,000 in contributions and $150,000 in earnings. She withdraws $100,000.

- Outcome: The entire $100,000 is tax-free because Jane is over 59½, and the account has been open for more than five years, making the distribution qualified.

Example 2: Non-Qualified Distribution of Contributions

Tom, age 48, has contributed $150,000 to his Roth IRA over the years, and the account has grown to $250,000. He withdraws $75,000.

- Outcome: The $75,000 comes entirely from his contributions, so it is tax-free and penalty-free, regardless of his age or the five-year rule.

Example 3: Non-Qualified Distribution of Earnings with Taxes and Penalty

Emily, age 45, has contributed $200,000 to her Roth IRA, and the account has grown to $300,000. She withdraws $250,000.

- Outcome:

- The first $200,000 (her contributions) is tax-free and penalty-free.

- The remaining $50,000 (earnings) is subject to ordinary income tax and a 10% early withdrawal penalty because Emily is under 59½ and does not qualify for any exceptions. Thus, she has to pay $5,000 in penalties on top of the income tax. In this case, she may be better off just withdrawing $200,000 as she is paying a price to withdraw the additional $50,000.

Example 4: Non-Qualified Conversion Distribution with Penalty

Mike, age 54, converted $500,000 from a Traditional IRA to a Roth IRA three years ago. He withdraws $100,000.

- Outcome:

- The $100,000 is not subject to income tax because Mike already paid taxes at the time of conversion.

- However, because the withdrawal is within five years of the conversion and Mike is under 59½, it incurs a 10% early withdrawal penalty ($10,000).

Example 5: Early Withdrawal with a First-Time Home Purchase Exception

Sarah, age 36, withdraws $100,000 from her Roth IRA to help buy her first home. Her account includes $60,000 in contributions and $40,000 in earnings.

- Outcome:

- The first $60,000 (her contributions) is tax-free and penalty-free.

- Of the $40,000 in earnings, $10,000 qualifies for the first-time homebuyer exception, avoiding the 10% penalty but subject to income tax. The remaining $30,000 is subject to income tax and the 10% penalty ($3,000).

Are You Dealing with a Roth IRA in Canada?

Common Questions About Taxes on Roth IRA Distributions

Are Roth IRA withdrawals taxable in Canada?

Roth IRA withdrawals may be taxable in Canada unless you file a treaty election under the Canada-U.S. Tax Treaty. With the election, qualified distributions are typically tax-free. Without it, earnings could be taxed as income. Professional advice is essential to navigate these complex cross-border tax rules.

Do Roth IRA distributions have to be reported on a tax return?

In the U.S., qualified Roth IRA distributions are not taxable and do not need to be reported. Non-qualified distributions or those involving earnings may require reporting. In Canada, distributions may need to be declared, depending on treaty elections and tax residency status.

What are the main Roth IRA withdrawal rules?

Withdrawals of contributions are always tax-free. For tax-free earnings, the account must meet the five-year rule, and you must be 59½ or meet exceptions (disability, first-time homebuyer, or death). Non-qualified distributions of earnings are subject to income tax and a 10% penalty unless exceptions apply.

What is a Roth IRA conversion?

A Roth IRA conversion involves transferring funds from a Traditional IRA or 401(k) into a Roth IRA. Taxes are due on pre-tax contributions and earnings at the time of conversion, but future qualified withdrawals from the Roth IRA are tax-free, making it a strategic planning tool.

When do I have to pay taxes on a Roth IRA withdrawal?

Taxes are due on Roth IRA withdrawals if the distribution is non-qualified and includes earnings. Contributions are always tax-free. Non-qualified earnings are subject to ordinary income tax and possibly a 10% penalty unless exceptions apply, such as for education expenses or a first-time home purchase.

What are the Roth IRA contribution limits?

In 2024, Roth IRA contribution limits are $7,000 ($8,000 if age 50 or older). These limits are reduced or eliminated if your Modified Adjusted Gross Income (MAGI) exceeds $146,000–$161 (single) or $230,000–$240,000 (married filing jointly). Income limits don’t apply to Backdoor Roth contributions.

Read the full rules for contributions on the IRS website HERE.

What is a Roth IRA?

Yes, a Roth IRA is a type of retirement account. Specifically, it is an individual retirement account (IRA) designed to provide tax advantages for retirement savings. Contributions to a Roth IRA are made with after-tax dollars, meaning you don’t get a tax deduction when you contribute. However, the key benefit is that qualified withdrawals during retirement are tax-free, including both your contributions and any earnings.

Are Roth IRA earnings taxable income?

Roth IRA earnings are not taxable income as long as they are withdrawn as part of a qualified distribution. However, if you take a non-qualified distribution of earnings, they will be subject to ordinary income tax and potentially an early withdrawal penalty unless an exception applies. Contributions, in contrast, are never taxable since they were made with after-tax dollars. Review the information above to find out if your withdrawal would be considered qualified.

Next Steps

If you’re a Canadian resident or are planning on moving to Canada or the US and need assistance with moving and optimizing your investments, estate planning, wealth management and portfolio management, please get in touch. At SWAN Wealth, we specialize in Canadian financial planning, cross-border financial planning and cross-border wealth management.

Read More

If you’re planning a cross-border move, these articles and guides will help simplify your move and ensure you’ve covered everything.

- Moving Your Roth IRA Account to Canada

- How to Transfer Your 401k to a Roth IRA while Still Employed

- IRA to Roth IRA Conversion

- 401(k) to IRA Rollover

About the Authors

Tiffany Woodfield is an Associate Portfolio Manager licensed in Canada and the USA, a Chartered Investment Manager (CIM), a Chartered Retirement Planning Counselor (CRPC), a Trust and Estate Practitioner (TEP) and the co-founder of SWAN Wealth Management, along with her husband, John Woodfield. Tiffany advises clients who live in Canada and the United States and want to simplify their cross-border financial plan, move their assets across the border, and optimize their investments to minimize their tax burden. Together, Tiffany and John Woodfield help their clients simplify their cross-border finances and create long-term revenue streams that will keep their assets safe whether they live in Canada or the U.S.

John Woodfield is a Financial Management Advisor (FMA), a Chartered Investment Manager (CIM), and a Certified Financial Planner (CFP), and in 2007 was inducted as a fellow of the Canadian Securities Institute (FCSI). As a portfolio manager and CFP®, he works with clients across Canada. John Woodfield’s clients are families, individuals and business owners who understand the importance of comprehensive wealth and investment plans driven by the lifestyle they want to lead.

Schedule a Call

Schedule a 15-minute introductory call with SWAN Wealth Management.

Click here to schedule a call.

![]()