How to Navigate U.S. Capital Gains Tax as Canadian Residents

Written by John Woodfield Portfolio Manager, CFP®, CIM® and Tiffany Woodfield, TEP, Associate Portfolio Manager, CRPC®, CIM®

If you are a U.S. person living in Canada—whether you're a Green Card holder, U.S. citizen, or dual citizen—understanding how to manage U.S. capital gains tax is critical.

The intersection of U.S. and Canadian tax rules can be confusing, with complexities that can lead to costly mistakes. This guide breaks down the essentials. It provides actionable strategies and emphasizes the importance of working with a cross-border financial advisor and accountant. This article is for information purposes only and you need to speak to an advisor and accountant about your particular situation.

Table of Contents

- Understanding Capital Gains Taxes: Canada vs. USA

- A Cross-Border Scenario: Timing Stock Options

- How the U.S.-Canada Tax Treaty Protects You

- Strategies to Minimize Tax Liability

- Estate Planning Considerations for Cross-Border Individuals

- Why You Need a Cross-Border Financial Advisor

- Q&A

Understanding Capital Gains Taxes: Canada vs. the U.S.

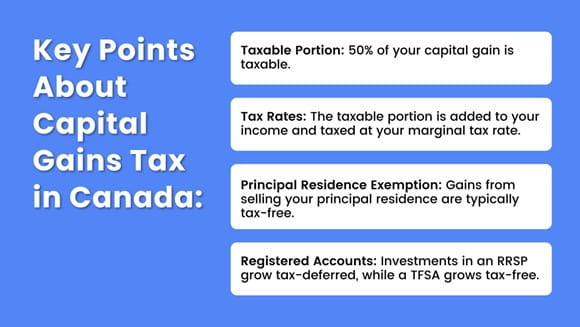

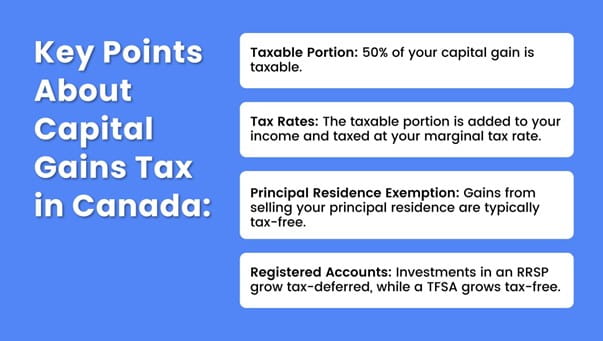

Capital Gains Tax in Canada

In Canada, capital gains are taxed on the profit you earn from selling stocks, bonds, real estate, or other investments. Here are the key points:

- Taxable Portion: 50% of your capital gain is taxable (e.g., on a $10,000 gain, $5,000 is added to your taxable income).

- Tax Rates: The taxable portion is added to your income and taxed at your marginal tax rate, which varies by province.

- Principal Residence Exemption: Gains from selling your principal residence are typically tax-free.

- Registered Accounts: Capital gains realized in an RRSP/RRIF grow tax-deferred and are 100% includable in income when withdrawn, while capital gains realized in a TFSA grows tax-free, helping you avoid capital gains taxes.

Capital Gains Tax in the U.S.

The U.S. has a tiered system based on how long you've held the asset:

- Short-Term Gains (held one year or less): Taxed as ordinary income, with federal tax rates from 10% to 37%. State income tax, if applicable, is in addition to the federal rates.

- Long-Term Gains (held over a year): Taxed at preferential federal tax rates of 0%, 15%, or 20%, depending on income. State income tax, if applicable, is in addition to the federal rates.

- Net Investment Income Tax (NIIT): An additional 3.8% may apply to higher earners.

- Primary Residence: You may exclude up to $250,000 ($500,000 for married couples) in gains from the sale of your home, provided you meet the criteria.

How the U.S.-Canada Tax Treaty Protects You

The U.S.-Canada Tax Treaty is designed to prevent double taxation, but it requires precise navigation. The treaty defines which country has primary taxing rights, depending on your residency and the source of the income. The country with secondary taxing rights may grant a foreign tax credit claim for taxes paid on the same income to the other country.

- Key Pitfalls: Not all taxes paid in one country are fully recoverable in the other, so meticulous planning is essential.

Strategies to Minimize Tax Liability

1 - Delay Realization of Gains

Taxes are only triggered when you sell an asset. Holding onto investments until you're in the lower-tax jurisdiction or lower tax bracket can save money.

2 - Use Tax-Advantaged Accounts

- Canada: RRSPs, TFSAs, and FHSAs shelter your investments from immediate taxation.

- USA: IRAs and Roth IRAs provide similar benefits, but coordination with Canadian tax rules is critical.

3 - Tax-Loss Harvesting

Selling investments at a loss can offset gains in the same tax year, reducing your taxable income. Excess losses can be carried forward in Canada. In the U.S. losses up to $3,000 are deductible against income and any excess may be carried forward.

Estate Planning Considerations for Cross-Border Individuals

For families with significant wealth and assets spanning Canada and the U.S., cross-border estate planning is not just important—it’s essential. Failing to plan effectively can result in unnecessary tax burdens and complications for your heirs. Here’s what you need to know:

U.S. Estate Tax

- Canadian and U.S. estates exceeding $13.99 million (as of 2025) may be subject to U.S. federal estate tax at rates of up to 40%. However, legislative changes could impact these limits.

- The estate tax exemption may be transferable to a U.S citizen surviving spouse, effectively doubling the threshold for married couples.

Canada’s Tax Rules

- While Canada does not impose an estate tax, assets are deemed sold at death, triggering capital gains tax on unrealized appreciation.

- Cross-border families must navigate both systems to ensure that tax-efficient strategies are in place for assets located in both countries.

Trusts for Cross-Border Families

- Trusts can play a vital role in minimizing estate tax and ensuring assets are transferred efficiently to the next generation.

- Properly structured U.S. or Canadian trusts can defer or eliminate taxes on inheritance while preserving privacy and control over wealth distribution.

- Beware of tax residency rules for trusts, as mismanagement can result in unintended tax consequences in both countries.

Life Insurance as a Tax Shield

- Life insurance policies are a powerful tool to fund estate taxes and provide liquidity, especially for U.S. assets subject to estate tax.

- In Canada, life insurance payouts are typically tax-free, making them an attractive option for covering cross-border tax liabilities.

By working with a dual-licensed cross-border advisor, and cross-border accountant you can design an estate plan that minimizes taxes, protects your wealth, and ensures a smooth transfer of assets to your heirs. A comprehensive strategy tailored to your unique situation is the cornerstone of effective cross-border estate planning.

Why You Need a Cross-Border Financial Advisor

Navigating the complexities of cross-border tax laws requires expert guidance. Here’s how a cross-border advisor can help:

- Tax Optimization: Avoid double taxation on investments by strategically planning for U.S. and Canadian tax obligations.

- Investment Management: Tailor your portfolio for tax efficiency in both countries.

- Compliance Support: Avoid costly penalties by staying compliant with IRS and CRA rules.

- Ongoing Guidance: As laws and financial goals evolve, your advisor ensures your plan stays on track.

Moving from the USA to Canada as an American - Critical Info!

A Cross-Border Scenario: Timing Stock Options

Meet Emma, a U.S. citizen working for a tech company in California. She has $700,000 in unexercised stock options and plans to move to Toronto in six months. Emma faces a critical decision:

- Exercise her options before moving, triggering U.S. income tax but avoiding Canadian tax.

- Wait to exercise in Canada, potentially subjecting her to higher Canadian tax rates and cross-border reporting requirements.

By consulting a cross-border advisor and accountant, Emma learns she can exercise her options before the move, obtain a higher cost basis in her shares, and significantly reduce her future capital gains tax liability.

Cross-Border Q & A

What is the Canadian tax liability for U.S. citizens or Green Card holders living in Canada?

Canadian tax liability refers to the taxes owed on worldwide income, including capital gains, by Canadian residents. U.S. citizens and Green Card holders must file U.S. taxes but may claim foreign tax credits to avoid double taxation.

What is the role of withholding tax when selling U.S. property as a Canadian resident?

Withholding tax ensures a portion of the sale proceeds is remitted to the IRS, acting as a prepayment against actual tax liability.

What does actual tax liability refer to?

Actual tax liability is the total amount of taxes you owe after applying deductions, credits, and prepayments such as withholding taxes.

What are the tax implications of owning foreign investment properties in the U.S. while residing in Canada?

Canadian residents must report rental income and capital gains from U.S. properties to the CRA and may owe U.S. taxes, offset by foreign tax credits. It also can expose Canadian’s to the U.S. estate tax.

How does the Canada Revenue Agency treat capital gains realized from U.S. property sales?

The CRA taxes 50% of capital gains realized on U.S. property sales, with foreign tax credits available for U.S. taxes paid on the same gains.

What steps can you take to minimize tax bills when paying capital gains tax in the U.S. and Canada?

Use tax treaties, claim foreign tax credits, time asset sales, and consult cross-border advisors to reduce double taxation.

What are the withholding tax rules under the U.S. Foreign Investment in Real Property Tax Act (FIRPTA)?

FIRPTA requires 15% of the sale price of U.S. real property owned by non-residents to be withheld at closing, subject to exemptions.

How do FIRPTA withholding tax rules impact Canadian residents selling U.S. real estate?

Canadian sellers face immediate withholding under FIRPTA but can file a U.S. tax return to recover excess withheld funds based on the actual tax owed.

When do Canadians pay tax on capital gains from investments held in the U.S.?

Canadians owe tax to the CRA on U.S. capital gains when the asset is sold, with foreign tax credits reducing double taxation.

What is the process for claiming a foreign tax credit for withholding tax paid to the IRS when filing Canadian taxes?

Report the U.S. withholding tax on your Canadian return, calculate your foreign tax credit, and apply it against Canadian taxes owed on the same income.

Final Thoughts

Managing U.S. capital gains tax as a Canadian resident is a complex but solvable challenge. The stakes are high, particularly for high-net-worth individuals navigating cross-border tax, investment, and estate planning. Working with a cross-border financial advisor and accountant ensures you receive the personalized guidance you need to minimize taxes, optimize investments, and achieve financial peace of mind.

If you’re ready to simplify your financial life across borders, reach out to a trusted cross-border advisory team today.

Next Steps

If you’re a Canadian resident or are planning on moving to Canada or the US and need assistance with moving and optimizing your investments, estate planning, wealth management and portfolio management, please get in touch. At SWAN Wealth, we specialize in Canadian financial planning, cross-border financial planning and cross-border wealth management.

Read More

If you’re planning a cross-border move, these articles and guides will help simplify your move and ensure you’ve covered everything.

- Financial and Tax Planning for US Citizens Living in Canada

- Getting Started Moving to the US from Canada

- What to Do With US Mutual Funds in Canada

- Renouncing US Citizenship: Pros and Cons

About the Authors

Tiffany Woodfield is an Associate Portfolio Manager licensed in Canada and the USA, a Chartered Investment Manager (CIM), a Chartered Retirement Planning Counselor (CRPC), a Trust and Estate Practitioner (TEP) and the co-founder of SWAN Wealth Management, along with her husband, John Woodfield. Tiffany advises clients who live in Canada and the United States and want to simplify their cross-border financial plan, move their assets across the border, and optimize their investments to minimize their tax burden. Together, Tiffany and John Woodfield help their clients simplify their cross-border finances and create long-term revenue streams that will keep their assets safe whether they live in Canada or the U.S.

John Woodfield is a Financial Management Advisor (FMA), a Chartered Investment Manager (CIM), and a Certified Financial Planner (CFP), and in 2007 was inducted as a fellow of the Canadian Securities Institute (FCSI). As a portfolio manager and CFP®, he works with clients across Canada. John Woodfield’s clients are families, individuals and business owners who understand the importance of comprehensive wealth and investment plans driven by the lifestyle they want to lead.

Schedule a Call

Schedule a 15-minute introductory call with SWAN Wealth Management. Click here to schedule a call.

![]()